BY ANTHONY KING

The chemicals sector in Europe has been squeezed hard over the past few years.

Globally, the chemical industry has been hit by weak demand and a slower recovery in manufacturing than predicted. High energy costs weigh heavily on the sector in Europe in particular, but so too has the ramp up of production capacity in China.

‘Energy costs are higher than levels prior to the outbreak of war in Ukraine and worsened an existing problem,’ says Sebastian Bray, head of chemicals research at Berenberg, an investment bank headquartered in Hamburg, Germany. ‘But overcapacity, stemming mainly from China, is the primary issue facing the European chemical sector right now.’

Part of the challenge for Europe is that in recent years China has built up huge capacities in petrochemicals. For some time the growth of production coming from China has put pressure on global prices and even triggered accusations of dumping. And experts warn that although the Iran war will likely see European facilities benefit from higher prices for some commodity chemicals, overall, the war might hurt European domestic demand and will not benefit Europe over the longer term. Meanwhile the US has been expanding in some areas, such as its ethylene capacity, thanks to its significant shale gas expansion. Europe, lacking either an advantage in raw materials or industry scale and costs, has been caught in the middle.

Bray foresees Chinese capacity coming back online after the Iran conflict ends or stabilises. ‘There’s not much for European chemicals to do but hunker down and hope for the best and increase prices where they can,’ says Bray.

Analysts say that China did not set out to flood the market. Its manufacturing sector was reliant on some chemical imports, and the Chinese Government made a push towards self-sufficiency. This has been a national imperative and broader economics is a secondary matter, says Richard Carter, an independent consultant for the industry.

‘They build because they don’t want to be beholden to massive imports,’ says Alasdair Nisbet, an M&A advisor to the chemicals industry at Natrium Capital.

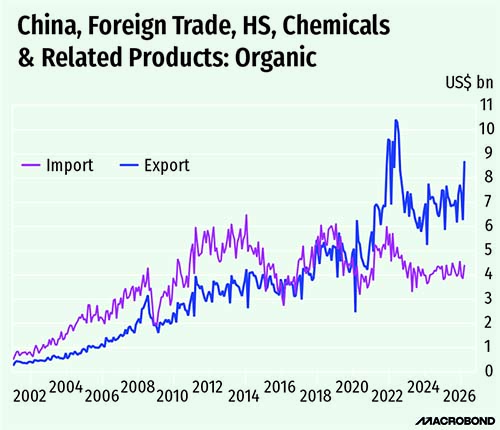

China had a capacity of 20mt of propylene capacity in 2015 (28% of global capacity) but added 3mt on average each year to hit 28mt in 2024, according to Argus Media. By 2034, almost half of global polypropylene capacity will be in China.

‘China has started exporting big volumes of polypropylene to neighbouring countries,’ says Dhanish Kalayarasu, a market analyst with Argus Media. The country followed a similar pattern in industrial machinery, photovoltaics and batteries, and more recently in electric vehicles.

China has become especially strong in value chains such as polyamides, polyurethanes, engineering polymers and some downstream intermediate chemicals such as butanediol. Yet it has not reached full self-sufficiency potential in major commodities such as polyethylene production and to date stayed out of more regional markets such as coatings and paints and industrial gases.

Chinese incentives

An important domestic driver for Chinese authorities is to build industries for job creation, crucial in a country with not much of a social safety net. ‘They are all about building stuff, manufacturing and employing people. That is how they boost their economy,’ says Steve Lewandowski, an olefins market expert at Chemical Market Analytics, a Dow Jones business unit. There has been a move to shut some smaller facilities and built state-of-the art plants. ‘Generally Chinese plants are modern, large scale and highly automated. As a result, they are extremely competitive,’ says Nisbet.

What seems to have happened is that Chinese production overshot demand, creating overcapacity in olefins and derivatives.

A recent Boston Consulting Group report noted that, since 2015, the growth in global capacity for bulk chemicals exceeded demand by 1% to 1.5%/year, something that is especially an issue for olefins and polyolefins production, squashing factory utilisation rates below 80% and into the red (C&I, 2025, 89, (11), 8). It was not the intention to deluge the global marketplace, say analysts. Rather the demand in the Chinese economy slackened, further weakened by a real estate downturn, and tentative consumer spending.

China’s chemical companies have some cost advantages over their European rivals. Carbon taxes and costs related to regulatory compliance are lower in China. Another important factor that can give Chinese facilities an edge is government subsidies. ‘Several aspects of energy costs, including the electricity price, are subsidised in China,’ says Bray. ‘And their domestic chemical producers, in my experience, often have greater tolerance for marginal profitability.’

Chinese firms can be more sanguine operating at a loss and can receive government support. In February 2026, the IMF called on China to cut its state support for industry, estimating that China spent around 4% of its GDP on assisting companies in critical sectors. ‘The number of zombie companies, defined as companies not able to pay interest on loans out of their revenue, is only increasing in green tech industry,’ says Alicia García-Herrero, an economist at Bruegel, a European economic think tank. She recently co-authored a report, Growth without profits: how will ‘involution’ in China end?

Involution is defined as intensive competition in overcrowded markets that results in price wars, reduced profit and resource allocation to ‘zombie firms.’ Even companies with productivity gains are lowering prices and add to a growing share of loss-making zombie firms, which live off bank support or government subsidies.

This has stoked tension between central government and regional governments inside the country. ‘China is very worried about involution,’ says García-Herrero. The solution for China lies in unproductive firms exiting the market. But regional governments want to maintain their own industries. Zombie firms ‘are not paying interest and the banks evergreen the loads,’ García-Herrero says.

It is not clear how influential involution is in the Chinese chemical sector. A steam cracker should run at around 85% capacity to break even and above 90% to return a healthy profit. It makes sense for Chinese facilities to run at close to maximum capacity and export a surplus. Meanwhile, European crackers run on average at 75% capacity. More plants in Europe will likely need to shut to restore operating rates.

Dark clouds

A report from European chemical industry group Cefic in January 2026 revealed that chemical plant closures in Europe have surged sixfold since 2022, hitting a cumulative 37mt of capacity – or around 9% of European production capacity – leading to the loss of 20,000 direct jobs in the chemical industry.

Another industry prediction warned that 1m direct jobs and another 10m jobs reliant on the chemicals sector for employment could be under threat. And the UK position also is not much better due to its sluggish economy. ‘The UK has to get over its own issues, such as lost GDP due to Brexit, low to zero growth and poor productivity, compared with European neighbours,’ says Carter.

The European Commission announced plans in October 2025 to boost competitiveness in the EU chemicals industry. Chemical company Ineos also criticised the Commission’s slow response to a surge of imports from China and filed 10 anti-dumping cases. It accused China of flooding Europe with carbon-intensive products that ‘pay a fraction of our energy costs and no carbon price at all’.

The Commission launched 162 anti-dumping actions, including 62 against companies in China, in 2024. Such investigations proceed in a slow legalistic manner and typically run for 12 to 15 months. The Commission’s actions have not buoyed sentiments in industry nor for market analysts.

‘There have been press reports on proposals to defer future increases in carbon taxes – a positive start. Yet absent China aggressively removing overcapacity, the real game changer would either be a more protectionist EU trade policy or very large energy subsidies in the bloc,’ says Bray. ‘With the exception of a handful of anti-dumping investigations, there is no evidence that the EU is prepared to do this.’

Some see more dark clouds on the horizon for the sector. ‘The industry is on the verge of collapse in Europe. The EU has not taken meaningful steps,’ says Lewandowski. ‘It has been neglectful in its approach to the chemical and petrochemical industry, and it’s going to come back to bite Europe because of the dependencies being created on imports.’

Even some economists think it is time to consider stronger measures. ‘We should have reacted years ago. Now we need tariffs to save European industry,’ says García-Herrero. She adds that China is worried about trade barriers, but also knows that Europe cannot close its market. Carter, an independent consultant, says that the Commission’s anti-dumping tariffs are often too targeted at individual firms and up until recently were too low. Carter says that even significantly higher tariffs, will not be enough to make a difference: ’But it will gain time,’ he says.

Others express pessimism, despite some steps by the Chinese government to rein in overcapacity, such as removing VAT rebates for certain chemicals such as polyvinyl chloride.

‘The action currently being taken is not yet enough to make a game-changing difference to a market that may be in oversupply for several years,’ says Bray. ‘Many observers will closely watch the next Chinese five-year plan for evidence that the government is willing to take further steps to address overcapacity.’

If China is faced with either cutting European industry some slack to relieve trade tensions or boosting employment, it will most likely prioritise domestic concern. Bray believes the most likely scenario is that European chemicals will be occasionally buoyed on news flows related to domestic political support or potential Chinese capacity rationalisations, ‘but meaningful change will take some time. It may take years to fully push the sector out of its rut.’ Already on the horizon is another looming problem for Europe: if the Iran war in the longer term might result in higher oil prices, this may crimp economic growth and further hurt the European chemical industry.