BY NEIL EISBERG

Brazil, the largest country in South America, is the world’s fifth-largest country by area and the seventh largest by population, home to over 213m people.

The country’s industrial output ranges from agriculture and food products, through aerospace, automotive and mining to chemicals and textiles. Chemicals represent 10-12% of GDP.

According to Brazilian chemical industry association, Abiquim, the Brazilian chemical industry ranks sixth in the world in terms of revenue, behind countries such as China, the US, Japan, Germany and South Korea.

The country has also recently welcomed the finalisation of the partnership agreement between four Mercosur countries (Argentina, Brazil, Paraguay and Uruguay) and the EU. This agreement is seen as an important milestone that expands the access of the chemical industry in Brazil to one of the largest markets in the world. The trade deal seeks to increase bilateral trade and investment, and lower tariff and non-tariff barriers - notably for small and medium-sized enterprises.

In Latin America, Brazil is the largest chemical market, leading the sector in the region. Abiquim, which represents about 750 companies, manufacturing more than 1500 chemical products, says this position reflects its diversified industrial capacity and its importance as a supplier of chemical products for various segments, such as agriculture, food, cosmetics and petrochemicals, all in all supporting around two million jobs.

Including all of its segments (industrial chemicals, fertilisers, personal hygiene, perfumery and cosmetics, pharmaceuticals, pesticides, soaps and detergents, paints, enamels and varnishes, artificial and synthetic fibres), the chemical industry in the country had an estimated net revenue of $187bn, in 2022.

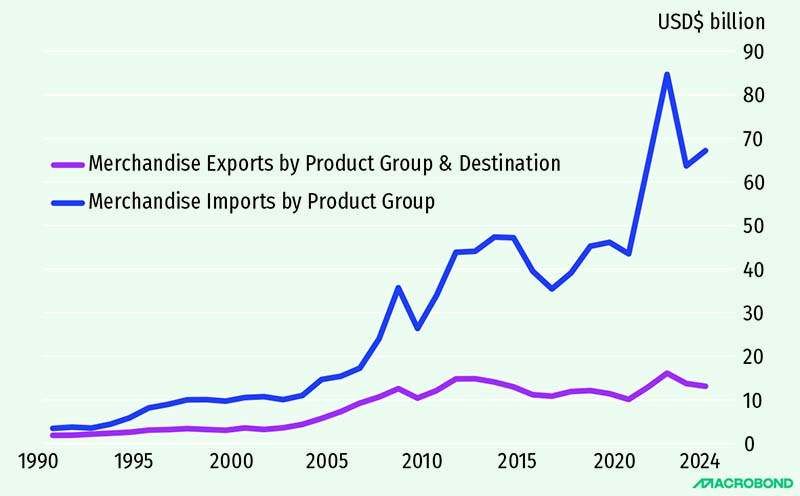

The net revenue of the industrial chemicals segment had an estimated value of $88.3bn in 2022. In 2022, Brazil exported $14.8bn in chemical products. But imports totalled $65bn, giving a deficit in the trade balance of $50.2bn.

According to industry figures, Brazil’s chemicals industry production grew 22.8% in the first three months of 2026, compared with end-2025, a significant boost after the decline in the second half of 2025, largely thanks to a fall in imports due to government efforts to protect the industry. This growth compares with GDP growth of just 0.9%.

‘Chemicals advanced more than twenty times that pace in terms of physical output. The difference is not just one of magnitude – it is one of direction,’ says Abiquim.

This current performance is undoubtedly positive, but it comes after a difficult time for the industry. In April 2025 Abiquim was warning that Brazil’s chemical industry was facing its worst performance in 30 years.

Imports represented 49% of total domestic demand, with significant increases in thermoplastic resins (28.3%), other inorganic products (26.7%) and organic chemicals (25.1%). The trade deficit had grown from $46.68bn in the previous twelve month period to $49.59bn. In contrast, back in 1990, only 7% of the national consumption of chemical products was met by imports.

The impact of these levels of imports was clear. The average plant idleness level was 40% in the first two months of 2025, the worst level recorded since 1990, according to Abiquim, but this hid some much higher levels including 61% for plasticiser intermediates, 48% for plastics intermediates and 44% for fertilisers.

To tackle the issue, late last year the Brazilian government passed the Special Program for Sustainability of the Chemical Industry (Presiq) with tax incentives designed to bring utilisation levels up to near full capacity, targeting 95% by 2030, as well as attracting low-carbon investments and the application of tax credits for the acquisition of less-polluting inputs and raw materials.

The incentives - linked to maintaining jobs and meeting targets linked to sustainability, innovation, and efficiency. If successful this could create 1.7 million direct and indirect jobs.

Market research consultant Mobility Forecasts predicts Brazil’s industrial chemicals market will grow from $780.4bn in 2025 to $1,045.7bn by 2031, with a CAGR of 5.0%. Demand growth is being driven by increasing industrialisation and urbanisation, resulting in growing demand for agrochemicals, pharmaceuticals and polymers.

Brazil could be described as the home of biofuels as it pioneered the development of bioethanol as an alternative for fossil-based vehicle fuels, and this work has extended into the production of other chemicals.

The minister of mines and energy, Alexandre Silveira, has recently proposed an increase in the mandatory blend of ethanol in gasoline to 32% (E32), up from 30% (E30). This has the potential to reduce gasoline imports by about 500m L/month, enough to make Brazil self-sufficient for the first time.

While Brazil’s bioethanol development has been focused on the use of agricultural biomass, mainly sugar cane, there are now plans to import used cooking oil (UCO), mainly from Asia, to produce sustainable aviation fuel (SAF).

Such imports are likely to be temporary, until other feedstocks with higher or similar added value become available. Alternative feedstocks, including soybean, corn oil and beef tallow, are possibilities for SAF production. Brazil currently produces 10,500 b/d of SAF, at the state-controlled Petrobras’ Duque de Caxias (Reduc) refinery. The country will produce 101,600 b/d by end-2026.

There are plans for two other refineries to produce SAF using alternative feedstocks such as canola and carinata oil seeds, at the Riograndense refinery in Rio Grande do Sul state, and yellow coconut oil at the Mataripe refinery, in Bahia state.

SAF production is understood to be aimed primarily for export, principally to the EU and US. Brazil does have a national aviation fuel program ProBioQAV that requires Brazilian airlines to systematically reduce greenhouse gas emissions in their domestic operations from 2027 by using SAF.

Impact of the Mercosur agreement

Abiquim points to the conclusion of the partnership agreement between Mercosur and the European Union, approved on January 9, 2026, (C&I, 2026, 90, (4), 9), and its implementation in April 2026, as a strategic milestone for the Brazilian chemical industry, by expanding access to one of the largest consumer markets in the world, stimulating investments, strengthening innovation and promoting a sustainability agenda.

‘The agreement represents a concrete opportunity to reposition the Brazilian chemical industry in global chains with higher added value. It expands access to markets, encourages technological exchange and creates a more predictable and modern environment for investments, especially in areas such as bioeconomy, renewable-based chemistry and clean energy,’ said André Passos Cordeiro, executive president, Abiquim.

‘By incorporating topics such as sustainability, intellectual property and fair trade, the agreement reinforces responsible practices and brings the Brazilian chemical industry closer to the requirements of the European market, which is fundamental for long-term competitiveness.’

Brazil, foreign trade, WTO merchandise trade values, manufactures, chemicals, total world, current prices, USD

Regulatory gaps

The Brazilian chemical sector is also in the midst of upgrades to its chemicals regulation. The adoption of Law No. 15.022/2024 aims to address these critical gaps in regulation and align Brazil with global standards for responsible chemical management.

Its requirements show some similarity with the EU Reach registration and authorisation procedures. Under the new legislation, chemical substances in the Brazil will be listed in a National Register of Chemical Substances, including data submitted by importers or manufacturers; and a National Inventory of Chemical Substances will be developed. Chemicals manufactured or imported in quantities of one tonne/year would will need to be registered in the National Inventory of Chemical Substances.

Just like EU Reach, this law and its implementation and compliance will require investment. The development of internal tools and procedures will be needed, and tests on substances may also be necessary, particularly, for new substances and those prioritised for risk assessment. Here, companies will be able to benefit from information and studies available from Brazilian and international institutions, as well as from risk assessment studies already carried out in other countries.

While the legislation entered into force in November 2024, the registration of substances will only be possible after the authorities develop the necessary systems, expected by November 2027.

Companies will then have three years to perform the registration.

Impact of Gulf crisis

The impact of the crisis in the Middle East has been broad and has been felt far and wide.

However, Abiquim says there is no risk of widespread chemical shortages due to the conflict in the Middle East, especially given exising idle capacity and the main sources of imports, the US, other countries in the Americas and China, are not operationally impacted by the conflict in the Middle East.

However, other product segments, such as methanol, nitrogen fertilisers and sulfur, depend more heavily on imports, while dependence on naphtha, which accounts for about 61% of the Brazilian production base, puts the country at a disadvantage in relation to international competitors, such as the US.